Cash-Secured Put Strategy: How to Sell Puts Systematically for Income

Selling a cash-secured put is one of the simplest options strategies. You agree to buy 100 shares of a stock at a specific price by a specific date. In exchange, you collect a premium upfront. If the stock stays above your strike, you keep the premium and move on. If it drops below, you buy the shares.

It's often described as "getting paid to place a limit order." That's accurate but incomplete. A limit order either fills or it doesn't. A cash-secured put has time value, delta exposure, implied volatility dynamics, earnings risk, and liquidity considerations. Treating it as a simple limit order leaves money on the table and exposes you to avoidable mistakes.

This guide breaks down how to evaluate and run cash-secured puts as a repeatable strategy, not a one-off trade.

How a Cash-Secured Put Works

You sell one put contract on a stock you'd be willing to own. Each contract represents 100 shares. You choose a strike price below the current market price and an expiration date.

You receive the premium immediately. In return, you're obligated to buy 100 shares at the strike price if the stock falls below it at expiration (or if the option is exercised early, though early assignment on puts is rare unless the stock collapses deep ITM near a dividend date).

"Cash-secured" means you have the full assignment amount in your account. Selling the $45 put means you have $4,500 set aside. This isn't margin — it's reserved cash. Your broker will hold it as collateral for the duration of the trade.

Three outcomes:

Stock stays above strike. The put expires worthless. You keep the premium. Your cash is released. You can sell another put.

Stock drops to or below strike. You get assigned. You now own 100 shares at the strike price, minus the premium collected. Your effective cost basis is the strike minus the premium — lower than what you would have paid with a limit order at the same price.

You close early. You buy back the put before expiration. If the stock has moved up or time has passed, the put is worth less than what you sold it for. You pocket the difference.

Why Most People Underestimate This Strategy

On the surface, cash-secured puts look conservative and boring. You're sitting on cash, collecting small premiums, and occasionally buying stock at a discount. Nothing flashy.

But when you run the numbers over multiple cycles, the math gets interesting.

Say you sell a $45 put for $1.10, 30 days to expiration. That's a 2.44% return on the $4,500 in committed capital, for one month. If you do this 10 times per year (accounting for some cycles where you get assigned and switch to covered calls), you're looking at roughly 20-25% annualized return on the cash — and that's on a strategy most people consider low-risk.

The catch is that annualized yield means nothing if one bad assignment wipes out six months of premiums. Which is why the setup selection matters more than the strategy itself.

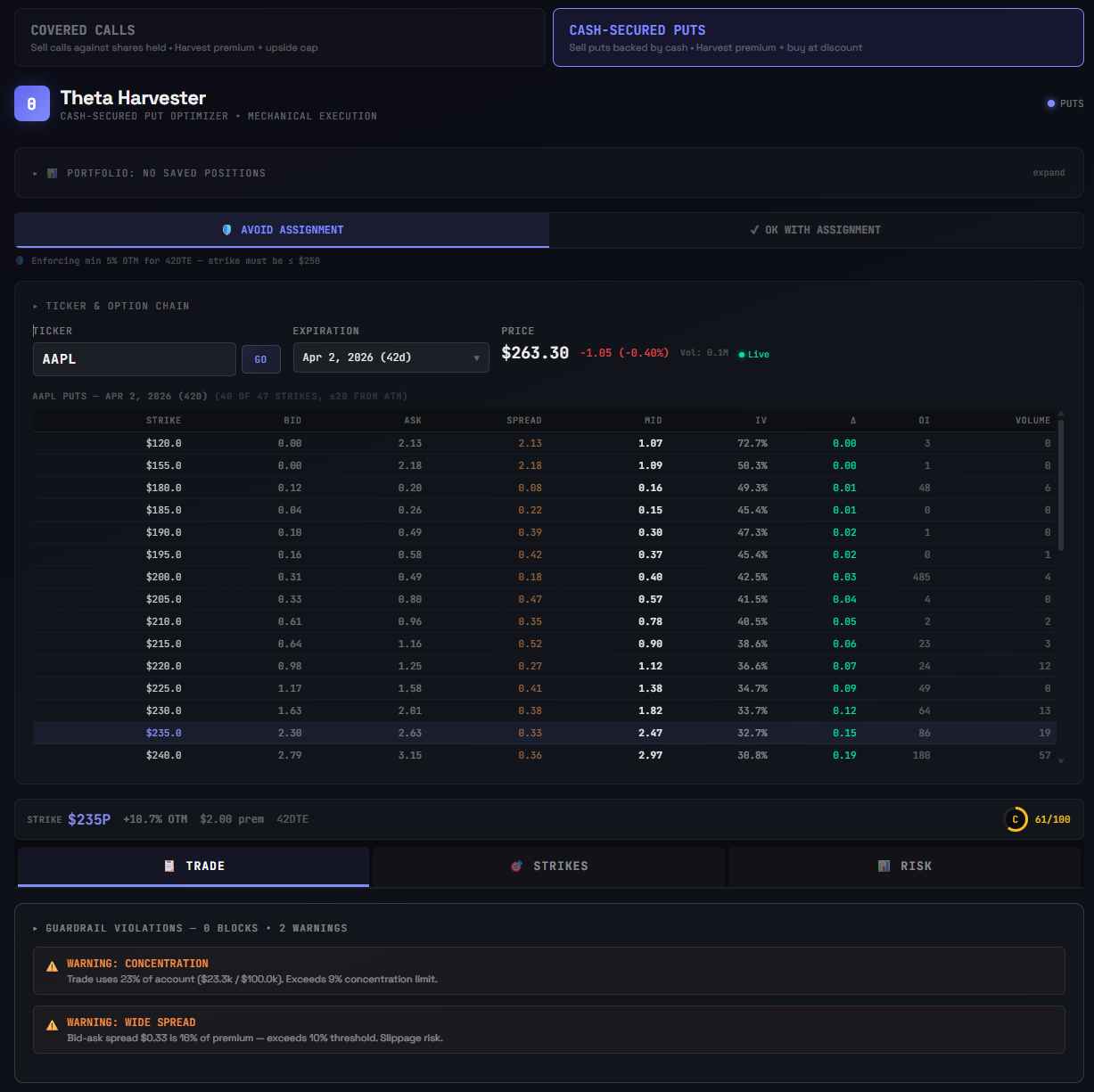

What to Evaluate Before Selling a Put

Every cash-secured put calculator will show you the premium, return if OTM, and breakeven. That's useful but it's not a decision framework. Here's what actually matters:

Would You Own This Stock at the Strike Price?

This is the filter that should come first. Not "does the premium look good" — but "if I get assigned, am I happy holding this stock at this price?"

If the answer is no, the premium is irrelevant. You're taking on assignment risk for a stock you don't want. That's speculation disguised as income.

The best cash-secured put candidates are stocks you'd buy anyway, at prices you'd buy them at anyway. The premium is a bonus for being willing to wait.

Delta: Your Probability Dial

Delta on a put approximates the probability of finishing in the money. A -0.20 delta put has roughly a 20% chance of assignment. A -0.30 delta has about 30%.

The tradeoff is direct: higher delta means more premium but more assignment risk. Lower delta means less premium but higher probability of keeping your cash free for the next cycle.

For most systematic sellers, the sweet spot is -0.20 to -0.30. You're getting meaningful premium without putting yourself in a coin-flip situation. Going below -0.15 and the premium often doesn't justify the capital lockup.

DTE: Time Decay Is Not Linear

Theta — the rate at which an option loses value over time — accelerates as expiration approaches. A 45-DTE put loses roughly the same amount of time value in its last 15 days as it does in the first 30.

This is why most systematic put sellers target 30 to 45 DTE. You're entering at the steepest part of the decay curve. You capture most of the time value erosion without sitting in the trade for months.

Shorter DTE (weeklies, 7-14 days) gives faster turnover but less premium per trade and tighter strike selection. Longer DTE (60-90 days) gives more premium but your capital is locked up longer and the annualized yield may actually be lower.

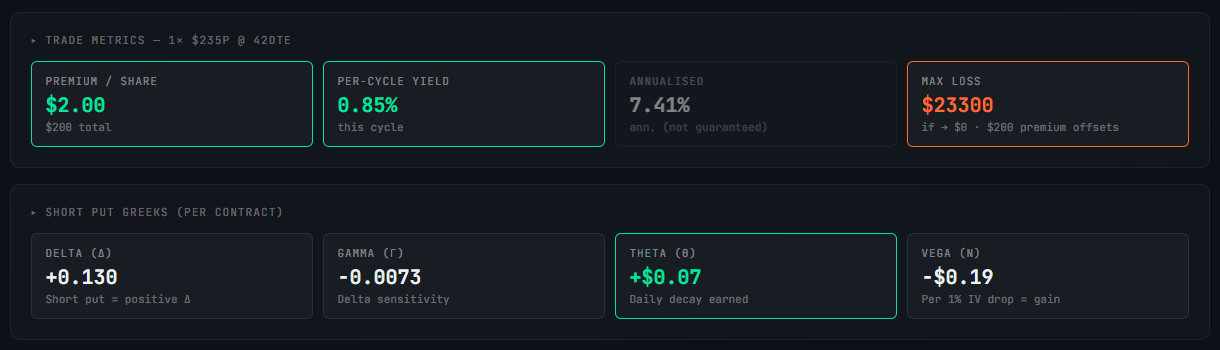

Premium Yield: The Number That Matters

Raw premium is meaningless without context. $0.80 sounds fine until you realize the strike is $200 and the DTE is 60 days. That's a 0.4% return over two months — roughly 2.4% annualized. Probably not worth locking up $20,000.

What you want is annualized yield on committed capital:

Premium ÷ Strike Price × (365 ÷ DTE) × 100

This normalizes every setup into the same unit: annual percentage return on the cash you're committing. Now you can compare a $0.80 premium on a $45 strike at 30 DTE against a $2.50 premium on a $150 strike at 45 DTE, and know which one is actually a better use of your capital.

A threshold of 15-25% annualized is reasonable for most market conditions. Below 10% and you're probably better off in a savings account. Above 40% and something else is going on — usually elevated IV from an upcoming binary event, which brings its own risks.

Bid-Ask Spread: The Hidden Cost

A put with a $0.80 mid-price and a $0.60/$1.00 bid-ask spread has a 50% spread. You're not getting $0.80. You're getting $0.65, maybe $0.70 on a good day. That shaves 10-15% off your expected yield before the trade even starts.

Spread width as a percentage of the mid-price is a quality signal. Under 10% is tight — large-cap, heavily traded names. 10-20% is workable. Over 25% and you're paying a meaningful tax on every entry and exit.

This matters even more if you plan to close early at 50% profit. You'll cross the spread twice — once to sell, once to buy back. Wide spreads compound the friction.

Open Interest and Volume

Open interest tells you how many contracts are outstanding at that strike. Volume tells you how many traded today. Both matter for fill quality and your ability to roll or close.

Below 50 open interest, you're in a thin market. Fills will be slow, slippage will be higher, and rolling later becomes a headache. Above 500 and you won't even notice the liquidity.

Earnings: The Binary Event

If earnings are inside your DTE window, everything changes. IV is elevated (which inflates premiums — tempting), but the stock can gap 10-20% on a miss. That premium you collected won't cover the drawdown.

There are two schools of thought:

Avoid earnings entirely. Select expirations that fall before the earnings date. Simpler, more predictable, fewer surprises. This is the safer mechanical approach.

Sell through earnings intentionally. Capture the elevated IV premium and accept the binary risk. This can work if the stock has a history of muted earnings moves and the premium compensates for the risk. But it's a conscious deviation from the standard playbook and should be flagged as such.

Either way, knowing when earnings fall relative to your expiration is non-negotiable. Getting blindsided by an earnings date you didn't check is an unforced error.

Building a CSP Grading System

With all these factors in play, evaluating a cash-secured put in your head is a recipe for inconsistency. Sometimes you'll weigh delta heavily, other times you'll fixate on premium. Your decision-making will vary with your mood, market conditions, and how your last trade went.

A grading system removes that. Each factor gets scored. The scores combine into an overall grade.

Premium yield — Is the annualized return above your threshold? Score higher for 20%+ annualized, lower for sub-10%.

Delta — Is it in your target range? Score highest at -0.20 to -0.25, lower at extremes.

Spread quality — How much are you losing to the bid-ask? Score higher for under 10%, penalize above 25%.

Liquidity — Enough open interest and volume to enter, manage, and exit cleanly?

Earnings risk — Are earnings inside the DTE window? If so, is the premium compensating for it?

Distance OTM — Is the strike far enough below spot to give you a buffer, or are you selling ATM and begging for assignment?

An A-grade setup has strong yield, appropriate delta, tight spreads, deep liquidity, and no earnings surprises. A D or F means one or more factors are critically weak — maybe you're chasing premium on a thin chain with earnings in two weeks.

The grade doesn't make the decision for you. But it turns a subjective "this looks OK" into an objective "this scores 82/100 with a flag on spread width."

Managing the Trade

Entering the trade is half the job. The other half is managing it.

Take Profit at 50%

If you sold a put for $1.00 and it's now worth $0.50, you've captured half the maximum profit with time still on the clock. Buying it back here frees your capital to sell another put.

Why not wait for full expiration? Because the last 50% of profit takes disproportionately more time and carries assignment risk that increases as expiration approaches. Taking 50% and redeploying is almost always better risk-adjusted than squeezing out the last few cents.

Roll When Tested

If the stock drops toward your strike with more than 7-10 days to expiration, you can roll — buy back the current put and sell a new one at the same strike or lower, further out in time. The roll should be done for a net credit (you receive more from the new put than you pay to close the old one).

Rolling isn't free money — you're extending your obligation. But it gives you more time for the stock to recover and you collect additional premium in the process.

Know Your Stop

Define your maximum acceptable loss before entering the trade. If the stock drops 20% below your strike, are you still happy holding? If not, set a rule: if unrealized loss on assignment would exceed X%, close the put for a loss and move on.

Having a stop doesn't mean you'll use it often. But not having one means a single bad trade can erase months of premiums.

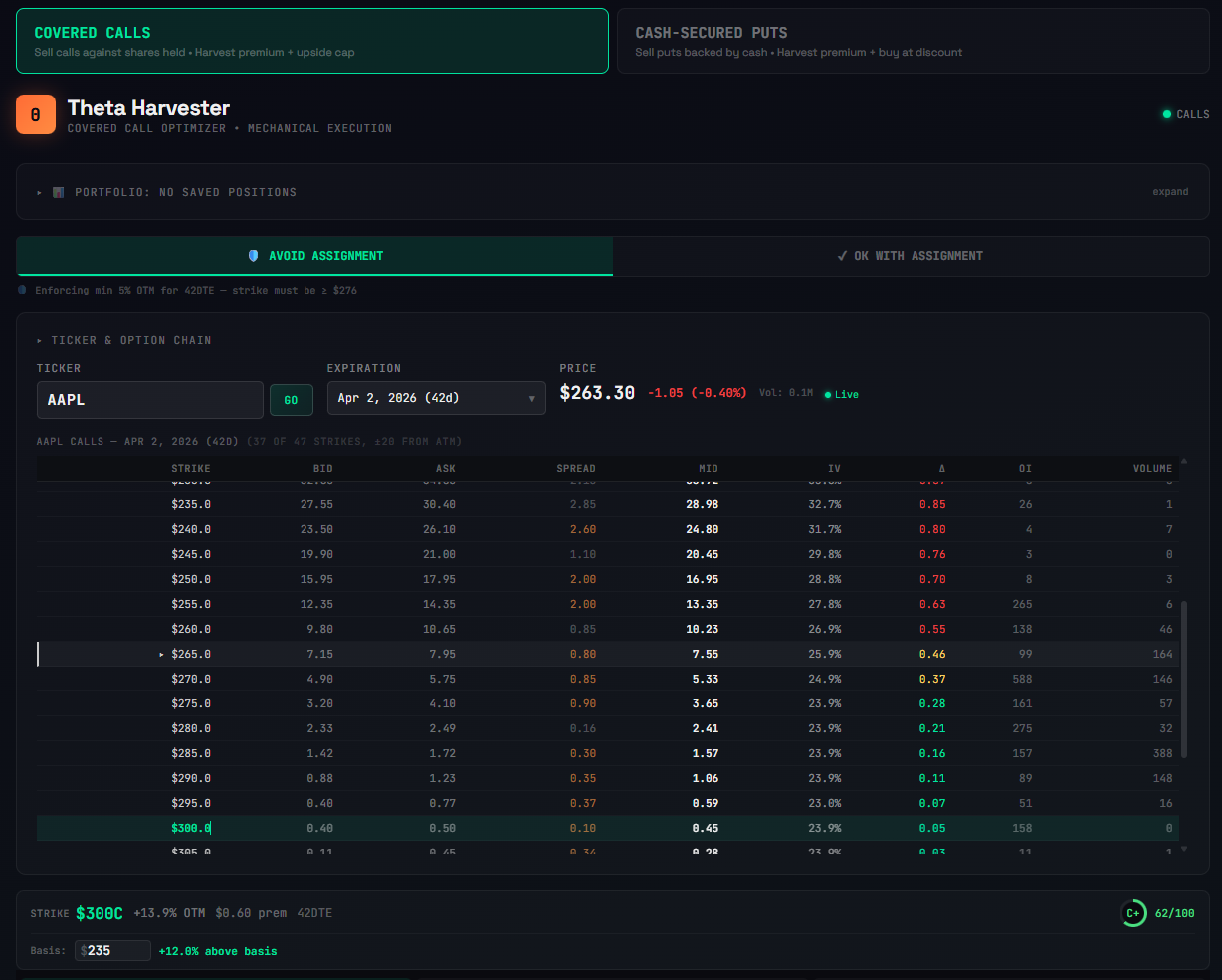

Cash-Secured Put vs Covered Call

Both strategies sell premium and both are theta-positive. The difference is your starting position.

With a cash-secured put, you start with cash and might end up with stock. With a covered call, you start with stock and might end up with cash.

In terms of risk profile, a cash-secured put at a given strike has nearly identical P&L to a covered call at the same strike on the same stock. The payoff diagrams overlap almost perfectly. The main differences are practical:

Capital efficiency. CSPs require cash collateral. Covered calls require stock. Depending on your account size and what you already own, one may be more capital-efficient than the other.

Assignment mechanics. Getting assigned on a CSP means buying shares. Getting assigned on a CC means selling shares. If you're running the wheel, these naturally flow into each other.

Tax treatment. Assignment on a CSP establishes a new cost basis. Assignment on a CC triggers a sale. Depending on your holding period and jurisdiction, the tax implications differ. This isn't trading advice — consult your tax professional.

For income-focused traders, the two strategies are best thought of as two phases of the same approach rather than separate strategies.

Try It Yourself

If you want to evaluate cash-secured puts systematically, ThetaHarvester grades every setup across delta, premium yield, spread quality, liquidity, and earnings proximity. You select a ticker and expiration, click a put strike, and get a letter grade with a full breakdown.

It also generates a management plan — when to take profit, when to consider rolling, and what to watch for — so you're not making reactive decisions mid-trade.

Free users can explore the full tool using demo tickers (AAPL, SPY, TSLA, NVDA, QQQ, MSFT). No signup form — just a magic link to your email.