Risk & Position Sizing for Options Sellers: Tail Risk, Kelly & Drawdown Math — Interactive

The fastest way to blow up selling premium isn't picking bad strikes. It's picking fine strikes at a size calibrated to the quiet months — and forgetting the rare claim.

Risk & Position Sizing is the fifth and final level of the Options School, and it exists because everything below it — the Greeks, the skew math, the wheel — is survivable knowledge only at the right size. The four simulators below are the live course widgets.

The Loss You Didn't Model

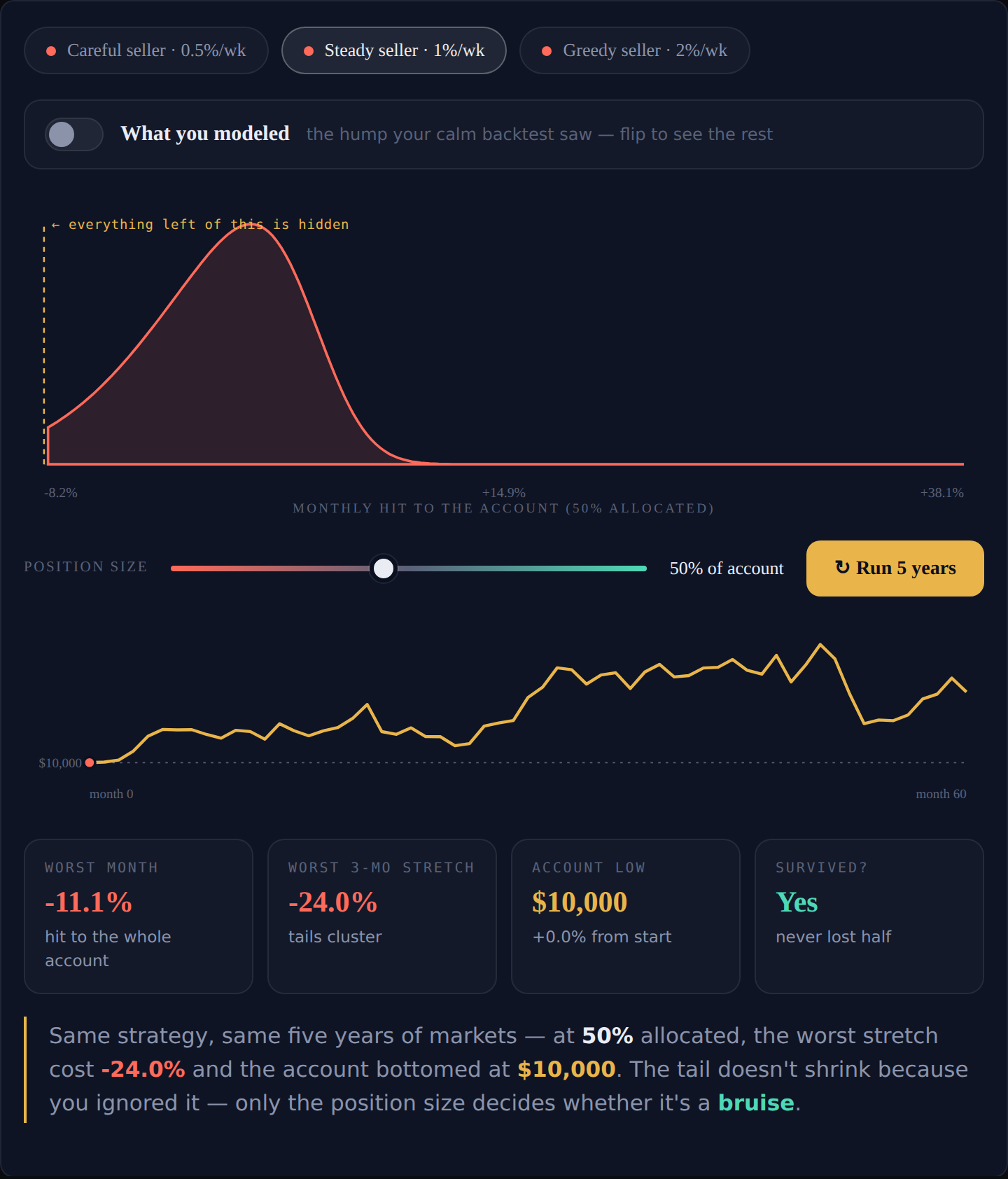

Premium-selling backtests are built from calm months — the visible hump of small wins — while the rare, oversized loss barely appears in the sample. The tail doesn't shrink because you ignored it; you just can't see it.

Short-premium tails have three engines that fire together: gap moves that jump straight through strikes (no stop-loss can exit at a price that never printed), correlations rising toward one so ten "diversified" short puts become one market bet, and IV spikes that reprice every short option against you at once.

The explorer from the Tail risk lesson hides the far-left tail behind a "what you modeled / what exists" toggle, then lets a position-size slider scale the damage:

The same five simulated years are a bruise at 20–30% of the account and an ending at 100%. Sizing is the only dial that changed.

The Over-Aggression Hump

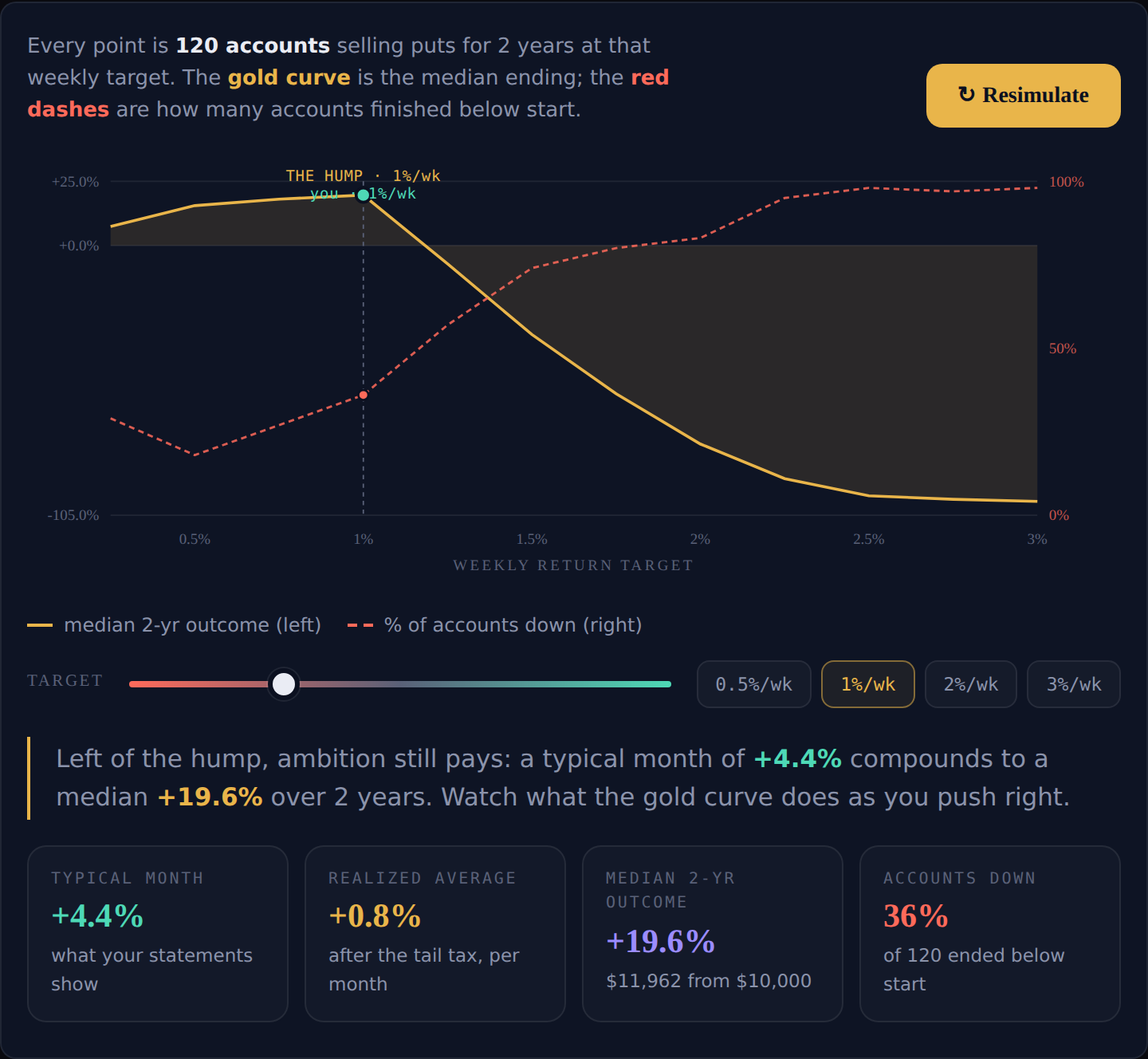

Here's the counterintuitive one. Sweep the weekly return target from 0.25% to 3%, simulate a couple hundred 2-year accounts at each step, and plot the median outcome. You don't get a rising line — you get a hump: median wealth rises with the target, tops out in the low fractions of a percent per week, then falls steeply.

The mechanism: a return target is a knob on your distribution, not just your income. Higher targets force closer strikes, shorter dates, and bigger size — and the loss tail grows super-linearly while the premium grows linearly. Past the hump, every extra point of ambition buys more tail than income.

Sweep it yourself in the simulator from the Over-aggression lesson:

The cruelest part: over-aggression is hard to self-diagnose because the feedback flatters you. The typical month stays exactly on target while the realized average sinks. Eight green months is what the losing configuration looks like from the inside.

Kelly and Optimal-f, Without the Algebra

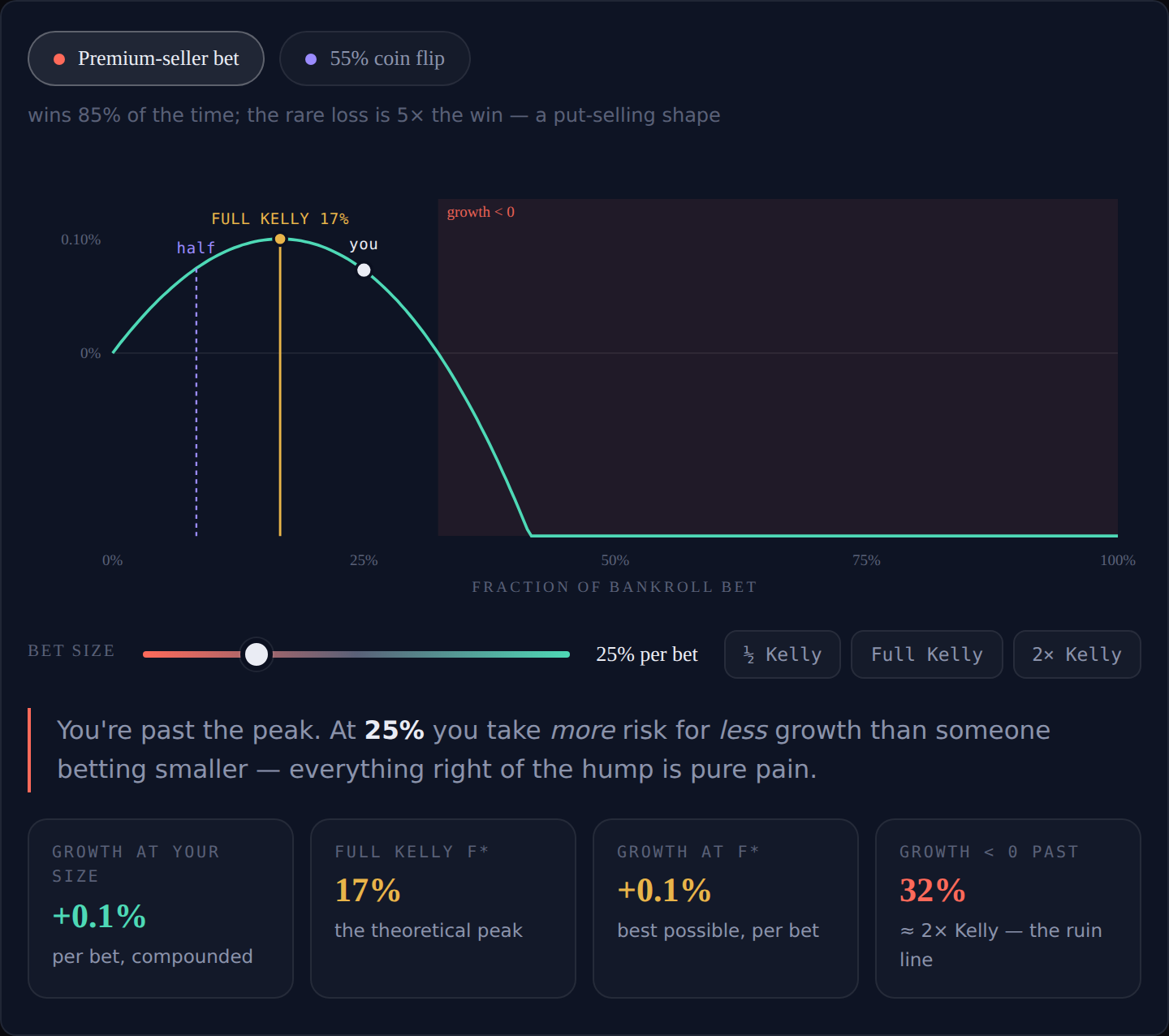

Compounded growth versus bet size is always a hump, never a line: bet 0% and earn nothing, bet everything repeatedly and the ruinous loss eventually arrives. The peak is full Kelly; gamblers call the same idea optimal-f.

The interactive bet in the Kelly lesson is shaped like premium selling: it wins 85% of the time, but the rare loss is 5× the win. Full Kelly lands near just 17% of the bankroll — and around 2× Kelly, the long-run growth rate crosses zero. Betting twice the optimum turns a positive-edge bet into a losing strategy through size alone:

Real traders run fractional Kelly: edges are estimated, unmodeled fat tails pull the true peak left of the computed one, and full-Kelly drawdowns (routinely ~50%) are deeper than most humans can hold. Half Kelly keeps roughly three-quarters of the growth for about half the swing.

Drawdown Math: The Asymmetry That Rules Everything

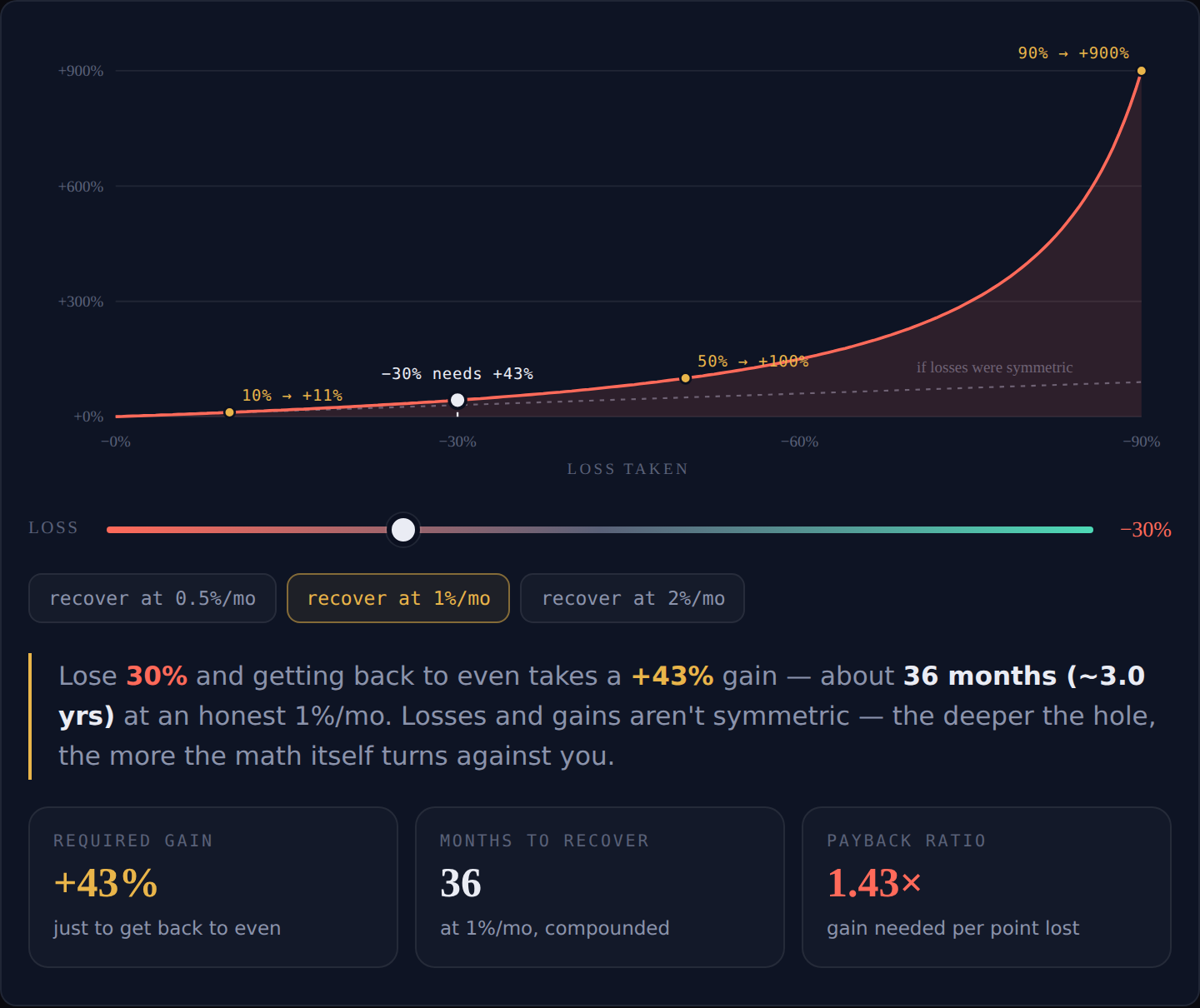

Lose 50% and you must gain 100% to get back to even, because the recovery is earned on the smaller base. The formula is required gain = loss / (1 − loss), and it accelerates viciously: 10% down needs +11%, 50% needs +100%, 90% needs +900%.

Calendars reveal what percentages hide. At an honest 1% per month, a 50% drawdown takes nearly six years of flawless compounding to unwind.

The final explorer, from the Drawdown math lesson, makes the asymmetry physical:

The capstone rule of the whole school: size every position so the worst plausible drawdown is one you can recover from — in money, in time, and in nerve — and then keep playing.

Take the Full Course

The Risk & Position Sizing course walks each idea with full prose and quizzes:

- Tail risk — the loss that isn't in your backtest

- Over-aggression — when higher targets lower returns

- Kelly & optimal-f — the growth hump and the 2× cliff

- Drawdown math — why a 50% loss needs a 100% gain

And this is the one level of the school that's directly wired into the tools: the Portfolio Allocator enforces per-trade R caps and single-name limits on your real book, and Theta Desk keeps the written rules these lessons tell you to pre-commit to. Learn the math, then let the machines hold you to it.