The Wheel Strategy Explained: How to Sell Options for Consistent Income

The wheel strategy is one of the most talked-about approaches to selling options for income. The pitch is simple: sell puts until you get assigned, then sell calls until your shares get called away. Rinse and repeat. Collect premium the entire time.

It sounds almost too clean. And in practice, it can be — if you run it mechanically and understand where the risks actually live.

The problem is that most explanations of the wheel stop at the diagram. They show you the loop but don't tell you how to pick the right strikes, when to adjust, or what happens when the underlying drops 25% and you're stuck holding shares with a cost basis well above the market.

This guide walks through the full wheel strategy — how each leg works, where the decision points are, and how to run it systematically instead of reactively.

What the Wheel Strategy Actually Is

The wheel has two phases that cycle back and forth:

Phase 1: Sell cash-secured puts. You pick a stock you'd be happy to own. You sell a put at a strike below the current price. You collect premium. If the stock stays above your strike, the put expires worthless and you keep the premium. If it drops below, you get assigned and buy 100 shares at the strike price.

Phase 2: Sell covered calls. Now you own 100 shares. You sell a call at a strike above your cost basis. You collect premium. If the stock stays below the strike, the call expires and you keep the premium. If it rises above, your shares get called away and you sell at the strike price.

Then you go back to Phase 1.

The appeal is that you're collecting premium in both phases. Whether you're waiting to buy or waiting to sell, theta is working for you. Your effective cost basis drops with every cycle because each premium collected lowers what you've paid (or raises what you'll receive).

Why People Get the Wheel Wrong

The diagram makes it look like a perpetual motion machine. Sell puts, collect premium. Get assigned, sell calls, collect premium. Get called away, sell puts again. Free money.

It's not. Here's where it goes sideways:

Ignoring Strike Selection

The most common mistake is picking strikes based purely on premium. A put with a fat premium at a strike 2% below spot is going to get assigned constantly. You'll end up owning shares you didn't really want at prices you didn't really like, and the premium you collected won't cover the drawdown.

Strike selection on the put side should be based on where you'd genuinely be happy buying the stock. Not where the premium looks juicy.

On the call side, the mistake is the opposite — selling calls too far out of the money to "protect" against assignment, collecting almost nothing in premium, and turning the strategy into a stock-holding exercise with a tiny income kicker.

Not Adjusting for Market Conditions

The wheel works best in range-bound or slowly trending markets. In a strong uptrend, your puts never get assigned and you're just collecting small premiums while missing the rally. In a sharp downtrend, you get assigned on the put and then the stock keeps falling — now you're selling calls below your cost basis or sitting on an unrealized loss waiting for a recovery.

Running the wheel identically in every market regime is a recipe for frustration. Your strike selection, DTE, and delta should shift based on volatility and trend.

No Exit Rules

What happens when the stock you got assigned at $45 is now at $32? Most wheel guides don't address this. Do you keep selling calls at $35 and lock in a loss if assigned? Do you wait for recovery? Do you cut the position?

Without predefined rules for these scenarios, you end up making emotional decisions — which is exactly what the wheel is supposed to prevent.

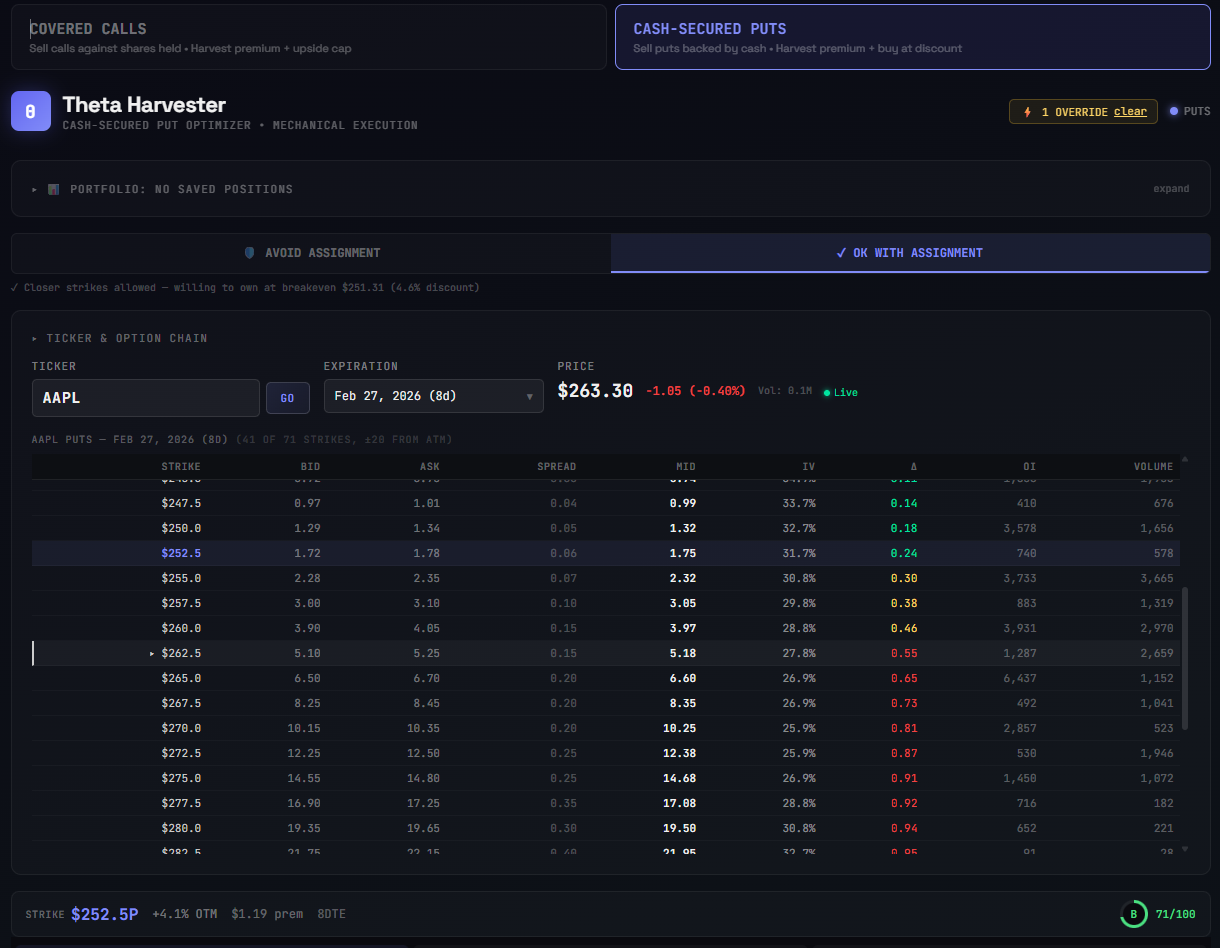

Phase 1: The Cash-Secured Put

The put side is where most wheel cycles start. You're looking at a stock you want to own, and you're willing to buy it at a discount.

Here's what matters:

Strike selection and delta. A 0.20-0.30 delta put gives you a reasonable probability of expiring out of the money (70-80%) while still collecting meaningful premium. Going lower — 0.10 delta — reduces assignment risk but the premium drops off steeply.

Think of the strike as your limit order with benefits. If you'd place a limit buy at $45 on a $50 stock, selling the $45 put is the same trade but you get paid to wait.

DTE. Theta decay accelerates in the last 30-45 days of a contract's life. Most systematic sellers target 30-45 DTE to capture the steepest part of the decay curve, then close at 50% profit or roll if needed. Weeklies offer faster turnover but less premium per trade and more frequent decision points.

Cash requirement. "Cash-secured" means you need the full assignment amount in your account. Selling the $45 put requires $4,500 in cash. This is capital that's locked up for the duration of the contract. The annualized yield on that locked capital is what you're optimizing for, not the raw dollar premium.

Premium yield. Collecting $1.20 on a $45 put for 30 days is 2.67% per cycle, or roughly 32% annualized. That's strong. Collecting $0.30 for the same strike and DTE is 0.67% per cycle — probably not worth the capital lockup.

Earnings. If the company reports earnings inside your DTE window, you're exposed to a binary event. The stock gaps down 15% on a miss and you're assigned well below where you expected. Some traders specifically avoid earnings. Others embrace the elevated IV. Either way, it should be a conscious decision, not a surprise.

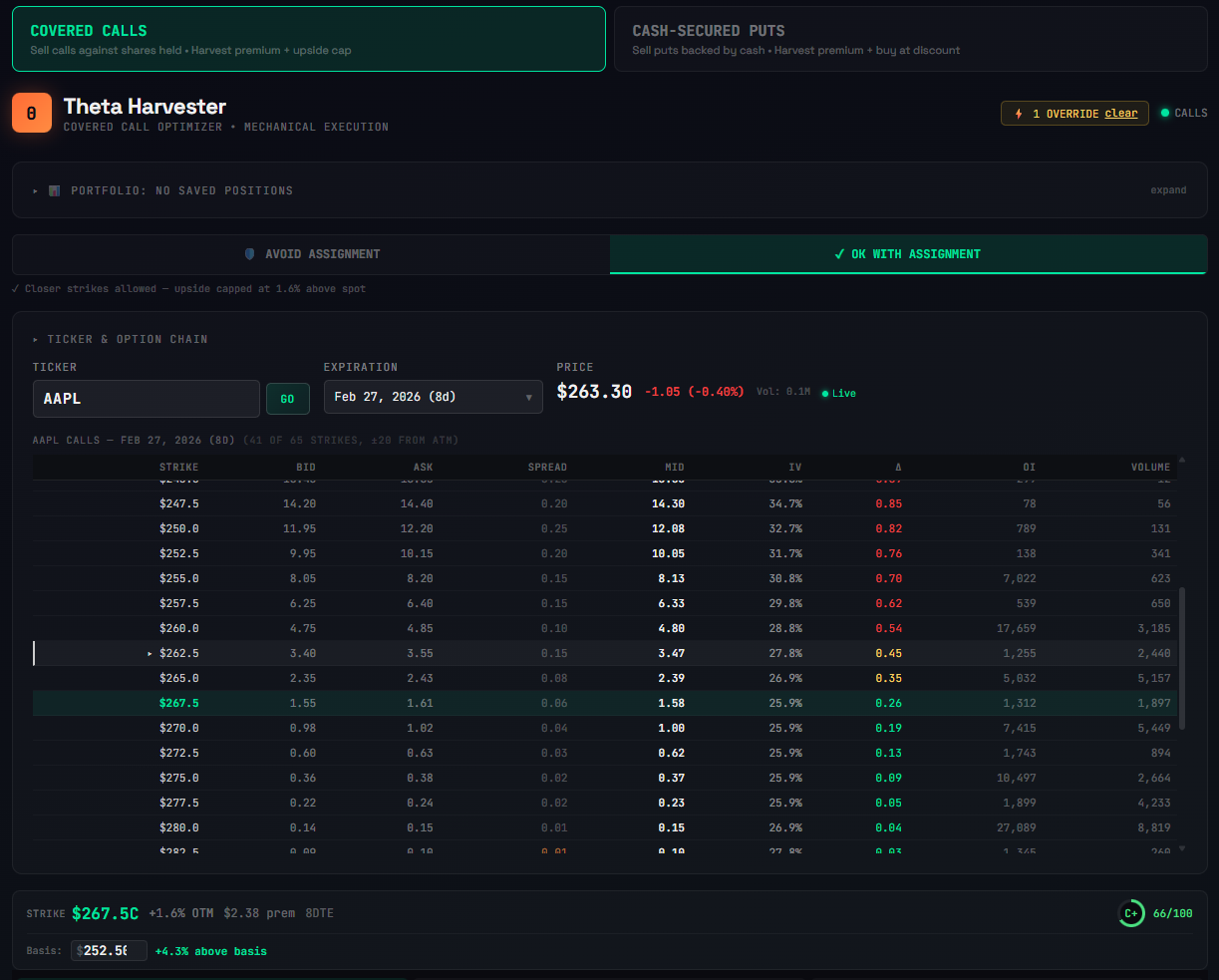

Phase 2: The Covered Call

You got assigned. Now you own 100 shares and you're in Phase 2.

The dynamics shift because now you have a cost basis and an unrealized position. Your goal is to collect premium while either holding for further upside or exiting at a profit.

Intent matters. Are you trying to get called away (exit the position at a profit) or are you trying to hold the shares and just collect income? This single decision determines your strike range.

If you want out, sell a call near your cost basis or slightly above. Higher delta, more premium, higher probability of assignment. If you want to hold, sell further OTM — lower delta, less premium, but you keep the shares more often.

Cost basis is your anchor. Never lose sight of it. If you were assigned at $45 and collected $1.20 in put premium, your effective basis is $43.80. Any call strike above $43.80 results in a net profit if assigned (including the original put premium).

Selling a call below your effective basis means you'd lock in a net loss if assigned. Sometimes this is the right move if the stock has dropped significantly and you want to exit — but it should be intentional.

The premium treadmill. Each call premium collected lowers your effective basis further. Assigned at $45, collected $1.20 in put premium, then sell a call for $0.85 — basis is now $42.95. Another cycle at $0.70 — basis is $42.25. The treadmill works in your favor as long as you're patient and the stock doesn't collapse.

Rolling. If the stock approaches or passes your call strike before expiration, you can roll — buy back the current call and sell a new one at a higher strike and/or later expiration. Rolling up and out gives you more room and more premium, but it's not free. The debit to close the current call eats into the credit from the new one. Track the net credit or debit of each roll.

Managing the Hard Parts

The wheel's sunny-day scenario is straightforward. The hard part is what happens when things don't go to plan.

The Stock Drops After Put Assignment

You sold a $45 put, got assigned, and now the stock is at $38. Your effective basis is $43.80. Selling covered calls at strikes above your basis means selling the $44 or $45 call — but with the stock at $38, those strikes have almost zero premium. You're stuck.

Options:

Sell calls below your basis. Accept a smaller net loss if assigned. If you sell the $40 call for $0.60, and the stock recovers to $40 and you get called away, your net P&L is: bought at $43.80, sold at $40.60 = -$3.20 per share. That's a loss, but a controlled one.

Sell calls at low delta and wait. The $44 call might pay $0.15. It's not much, but it chips away at your basis each cycle. This requires patience and conviction that the stock will eventually recover.

Cut the position. Sell the shares, take the loss, go back to Phase 1 on a different ticker. This feels like failure but sometimes it's the right move. A defined loss is better than an indefinite drawdown. Set a maximum loss threshold before you enter the wheel — e.g., if unrealized loss exceeds 20% of assignment value, exit.

The Stock Rips After Call Assignment

You sold a $50 covered call, the stock went to $60, your shares got called away at $50. You "missed" $10 of upside. This is the most common complaint about the wheel.

Here's the thing: you made money. You collected put premium on the way in, call premium while holding, and sold at or above your basis. The regret is real but the P&L is green. If you keep chasing upside, you're not a theta seller — you're a stock picker who sometimes sells options.

The mechanical response is simple: go back to Phase 1. Sell a put on the same stock or a different one. Don't chase.

Low Volatility Environments

When IV compresses, premiums shrink across the board. The wheel still works but the yields are lower. This is when discipline matters most — don't stretch for premium by selling higher-delta puts or tighter calls. Accept the lower yield or sit on cash until conditions improve.

Running the Wheel Mechanically

The whole point of the wheel is repeatability. Take the decision-making out of each step and replace it with rules.

Here's a framework:

Entry rules for puts:

- Stock is one you'd own at the strike price (not just for the premium)

- Delta between 0.20 and 0.30

- DTE between 30 and 45 days

- No earnings inside the DTE window (or conscious decision to include them)

- Bid-ask spread under 15% of premium

- Open interest above 100

- Annualized yield above your threshold (e.g., 15%)

Entry rules for calls:

- Strike above effective cost basis (unless intentionally exiting at a loss)

- Delta appropriate for intent: 0.25-0.40 if seeking assignment, 0.15-0.25 if holding

- Same DTE, spread, and OI criteria as puts

- Check earnings — same risk applies

Management rules:

- Close at 50% of premium collected (take the win, redeploy capital)

- Roll if the position goes ITM with more than 7 days to expiration

- Maximum loss stop: if unrealized loss on assigned shares exceeds your threshold, exit

- Track effective cost basis after every cycle — it's your scoreboard

Position sizing:

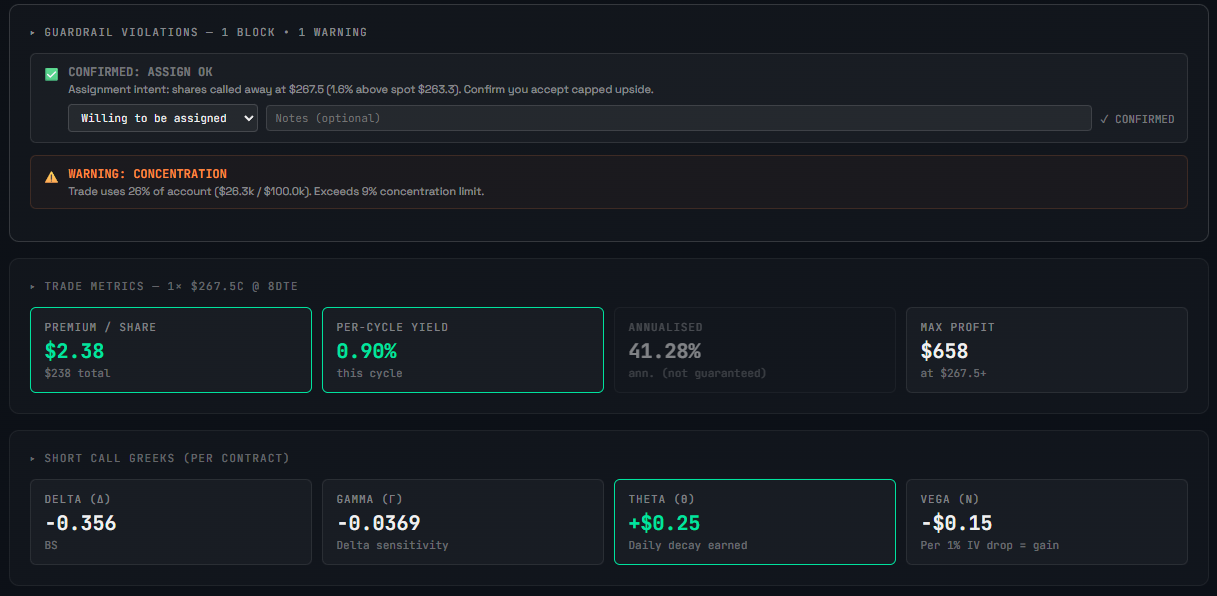

- Never commit more than 20-25% of your account to a single wheel position

- Keep enough cash to handle two simultaneous assignments if you're running multiple wheels

The Real Edge

The wheel doesn't have an edge because of some secret sauce. The edge is consistency. You're selling time decay to people who are buying lottery tickets. Most of those tickets expire worthless. Over hundreds of cycles, the math works in your favor — as long as you don't blow up on any single position.

That means the grading process matters more than any individual trade. Every put you sell, every call you write, should pass through the same checklist. Delta, yield, spread, liquidity, earnings, position size. If it doesn't qualify, you don't trade.

Try It Yourself

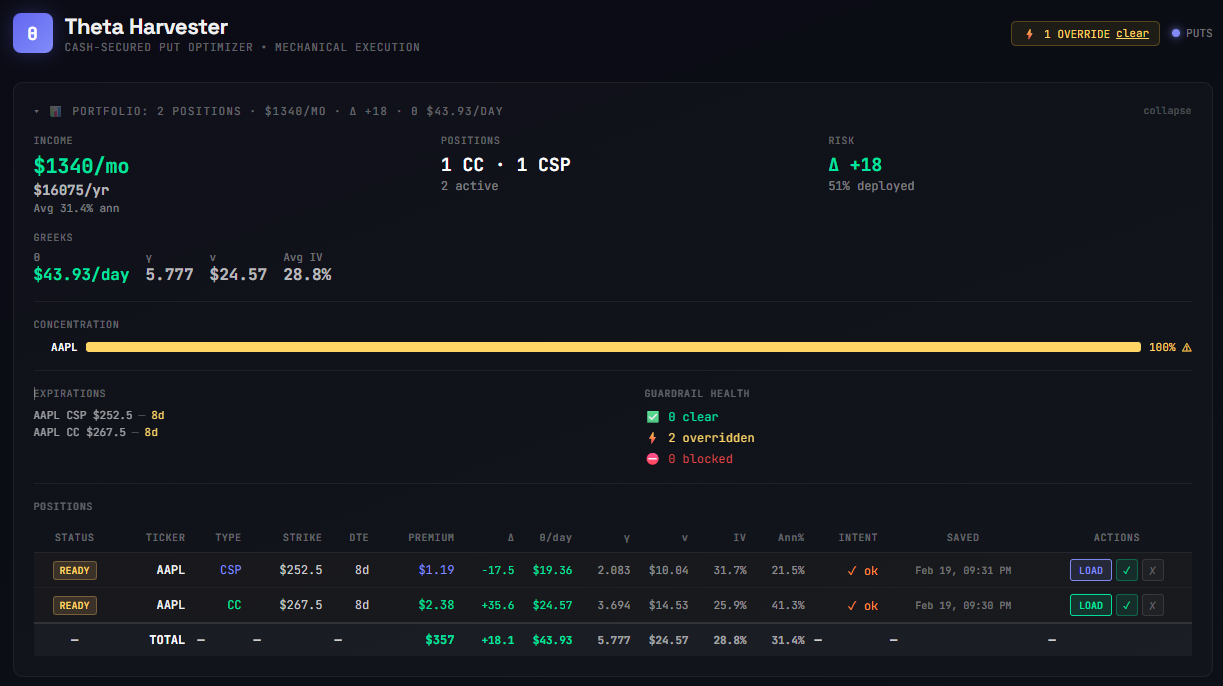

If you want to run the wheel mechanically, ThetaHarvester can help. It grades both cash-secured put and covered call setups across delta, premium yield, spread quality, liquidity, and earnings proximity — then generates a management plan with take-profit and roll triggers.

You can save each position to a portfolio view that tracks your aggregate theta income, effective cost basis, and Greeks exposure across all your wheel positions.

Free users can explore the full tool using demo tickers (AAPL, SPY, TSLA, NVDA, QQQ, MSFT). No signup form — just a magic link to your email.