The Option Greeks, Explained Interactively: Delta, Theta, Vega, Gamma

The Greeks are where most options education loses people. Four letters, four partial derivatives, and a wall of textbook definitions that evaporate the moment a real position moves against you.

The Greeks course in the Options School takes a different approach: one Greek per lesson, one interactive figure per Greek, and every number tied back to the premium seller's actual job. The explorers below are the real course widgets — live, not screenshots.

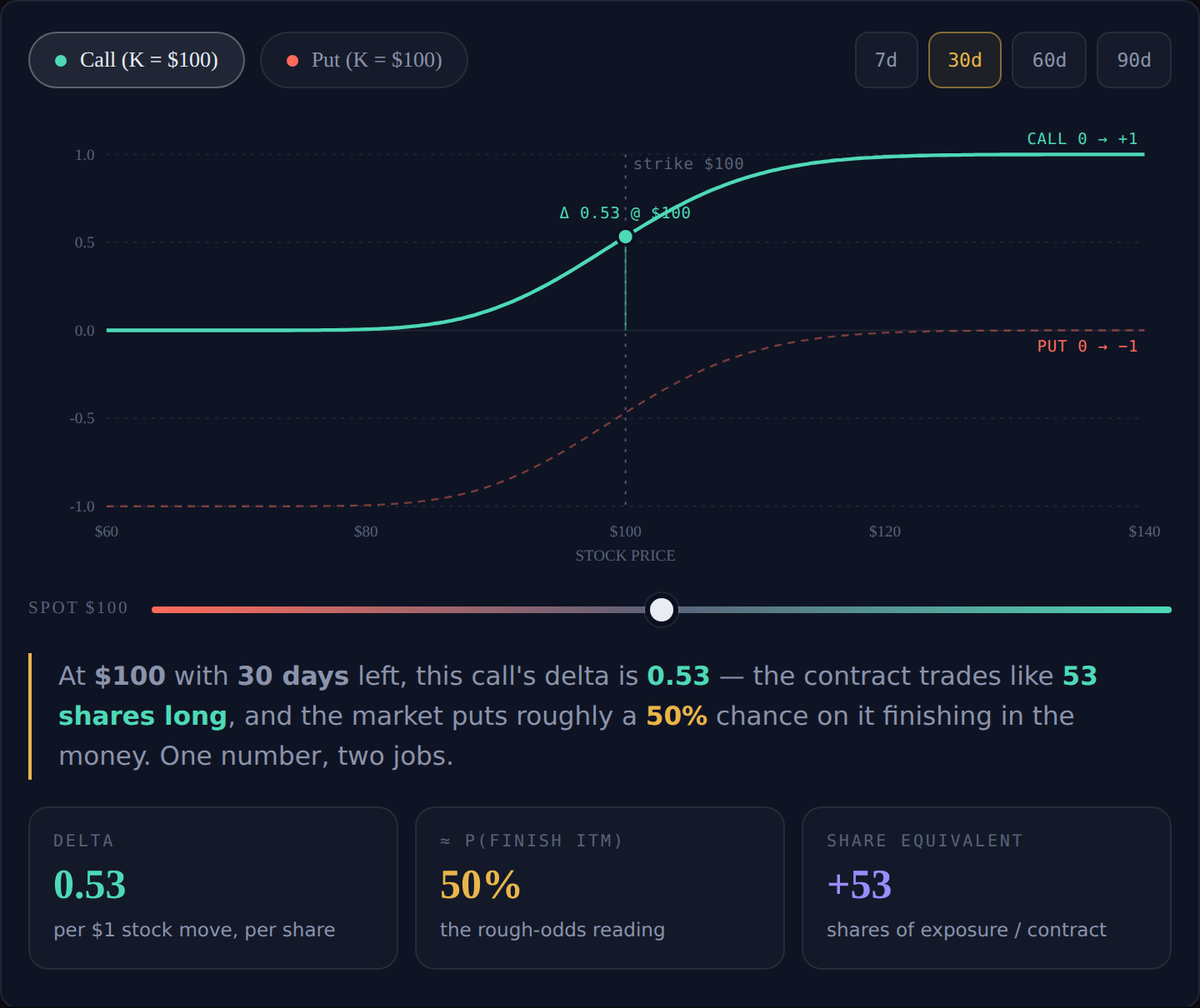

Delta: One Number, Two Jobs

Delta is how much an option's price changes per $1 move in the stock — a volume knob on direction. Call deltas run 0 to +1, put deltas 0 to −1, and one contract's delta × 100 is its share-equivalent exposure: a 0.62-delta call trades like 62 shares.

Delta's second job is the odds shortcut: it approximates the probability the option finishes in the money. A 0.30-delta put carries roughly 30% assignment odds — which is exactly why premium sellers quote strikes in delta instead of dollars.

This is the delta explorer from the Delta lesson. Drag the spot price, switch days-to-expiry, and watch the S-curve and the live stats respond:

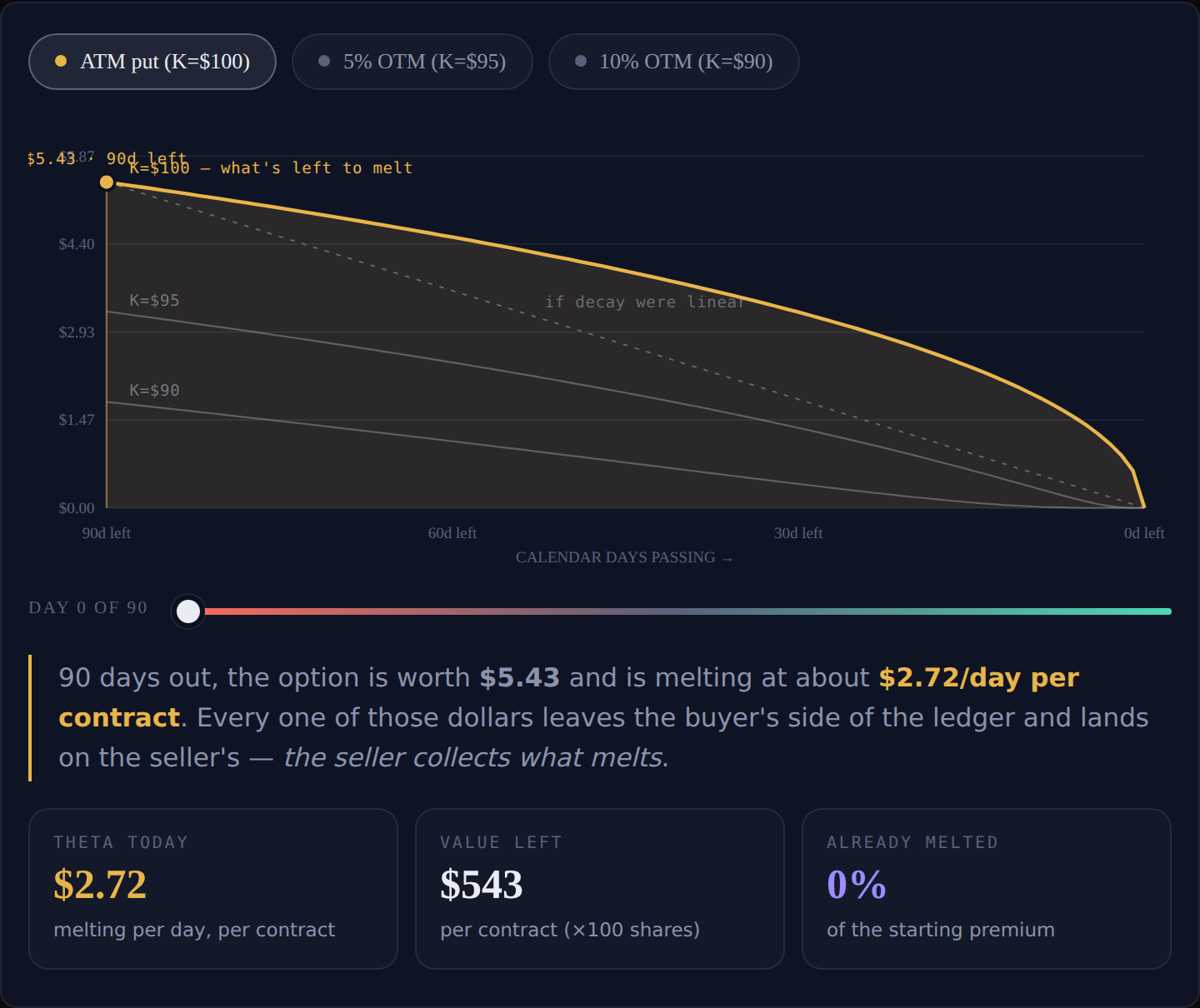

Theta: The Harvest

Theta is how much an option's price falls per day, all else equal — and for the seller it's the paycheck. It only ever eats extrinsic value: each quiet day moves real dollars from the buyer's ledger to the seller's.

The shape of the decay curve is the seller's edge. At-the-money extrinsic value scales with the square root of time, so decay accelerates into expiry — the last 30 days melt more than the first 30, and the final week melts fastest. That geometry is why sellers cluster entries in the 30–45 DTE window.

Run the clock yourself — this is the decay curve from the Theta lesson. Slide days elapsed, switch between ATM and OTM strikes, and watch theta per day and percent melted update:

Notice what OTM strikes do: their small premium bleeds out early and flattens. The juicy acceleration belongs to the at-the-money strike — which, as the gamma lesson explains, is no coincidence.

Vega: Why Your Option Lost Money While the Stock Went Up

Every option trades in two markets at once: the stock's price, and the market's forecast of how much it will move — implied volatility. Vega is your exposure to the second market.

The classic ambush is the earnings IV crush. Pre-report options carry inflated IV; when the news lands, the uncertainty is spent and IV collapses — so a buyer can be right on direction and still lose, because the vega loss outweighs the delta gain.

Stage the crush yourself in the explorer from the Vega lesson — park IV high, collapse it, and read the damage across expiries:

For premium sellers the punchline is structural: selling a cash-secured put or covered call is selling volatility. The persistent gap between implied and realized volatility — covered in depth in the IV vs realized lesson — is a large part of why the harvest exists at all.

Gamma: The Hidden Accelerant

Gamma is the Greek of the Greek: how fast delta itself changes per $1 of stock move. Near expiry it becomes the accelerant — delta must resolve to 0 or 1 at the bell, so the smooth S-curve sharpens into a step at the strike. ATM gamma runs about 0.05 per dollar at 30 days, ~0.10 at 7 days, and roughly 0.25 with one day left.

Morph the curve yourself — the explorer from the Gamma lesson runs the S-curve from 90 days down to 1:

The lesson's core is the theta/gamma coin: you are paid theta precisely for carrying gamma risk, and both concentrate in the same place — at the money, near expiry. The seller's 30–45 DTE entry window and close-early rules are gamma management in disguise: the last slice of premium into expiry week is the most expensive to earn.

Take the Full Course

All four explorers come from the Greeks course — free, quizzed, and built for premium sellers:

- Delta — direction, share equivalence, and ITM odds

- Theta — the harvest and the decay curve's shape

- Vega — IV crush and why selling premium is selling vol

- Gamma — the accelerant you're paid to carry

New to the instrument itself? Start one level down with Foundations. Ready to put delta to work picking strikes? The setup grader scores your delta positioning on every covered call and CSP — and the Monte Carlo simulator shows you what those odds mean over 12 months.