The Portfolio Allocator: Sleeve-Based Capital Allocation for Options Sellers

Grading a single trade is a solved problem — that's what the setup grader is for. But there's a second question that no single-trade tool can answer:

How much of your account should be selling premium right now, and is this next trade the one that pushes you over?

Most options sellers never answer it explicitly. They size trades one at a time, each one reasonable on its own, and let the portfolio happen by accident. Then a volatility spike marks every short put underwater at once, and the "diversified" book turns out to be one big short-vol bet.

The Portfolio Allocator is the ThetaHarvester engine built for that book-level question.

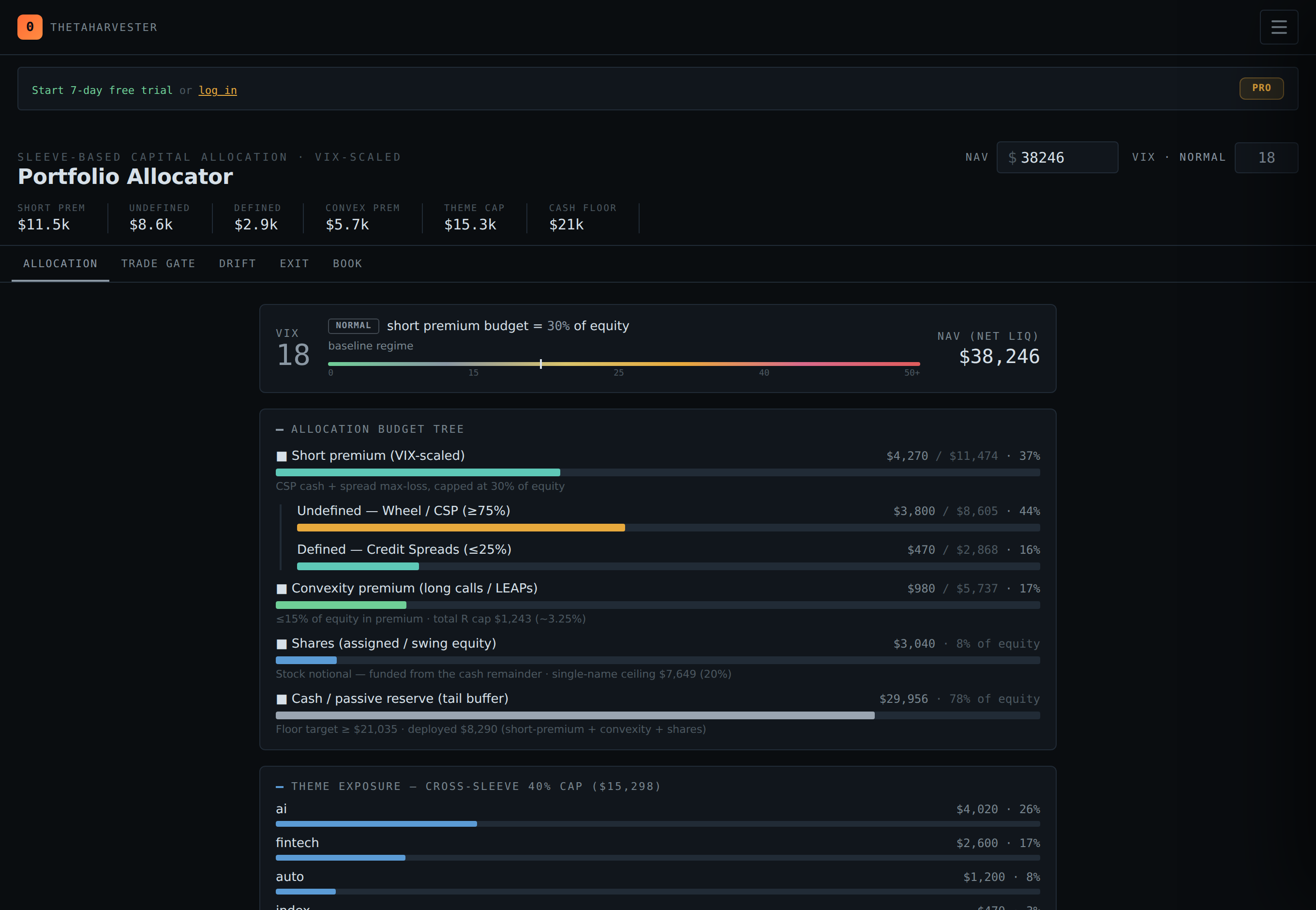

The Sleeve Framework

The allocator organizes your book into four sleeves, each with a defined risk class and role:

- Wheel / CSP — cash-secured puts. Undefined risk, core income.

- Credit Spreads — defined risk, core income, strictly capped.

- Long Convexity — long calls and LEAPs. Long premium, supplemental — the positive-skew counterweight to the income sleeves.

- Shares — the equity that assignment leaves behind, plus deliberate swing positions.

The framework's backbone is the classic capital-allocation playbook from the tastytrade / Spina school — core versus supplemental, undefined versus defined risk, per-position buying-power caps — reconciled with the per-sleeve SOPs from Theta Desk.

The VIX Decides Your Budget

The allocator's headline number is the short-premium budget: the slice of your account allowed to be committed to premium selling. It isn't fixed — it scales with the VIX:

- VIX under 15 (Calm) — 25% of equity. Premium is scarce; don't reach for it.

- VIX 15–20 (Normal) — 30%

- VIX 20–25 (Elevated) — 35%

- VIX 25–30 (Stressed) — 40%

- VIX 30–40 (High) — 45%

- VIX 40+ (Crisis) — 50%. Rich premium, maximum allocation.

This inverts what most sellers do instinctively. When markets are calm and premium is thin, the budget forces you small — exactly when reaching for yield means selling closer strikes for less money. When volatility spikes and everyone else is panicking, the budget expands — because that's when the variance risk premium is fattest.

Within the short-premium budget, a second split is enforced: at least 75% undefined risk (CSPs), at most 25% defined risk (spreads) — plus a cash reserve floor computed from whatever the budgets don't claim.

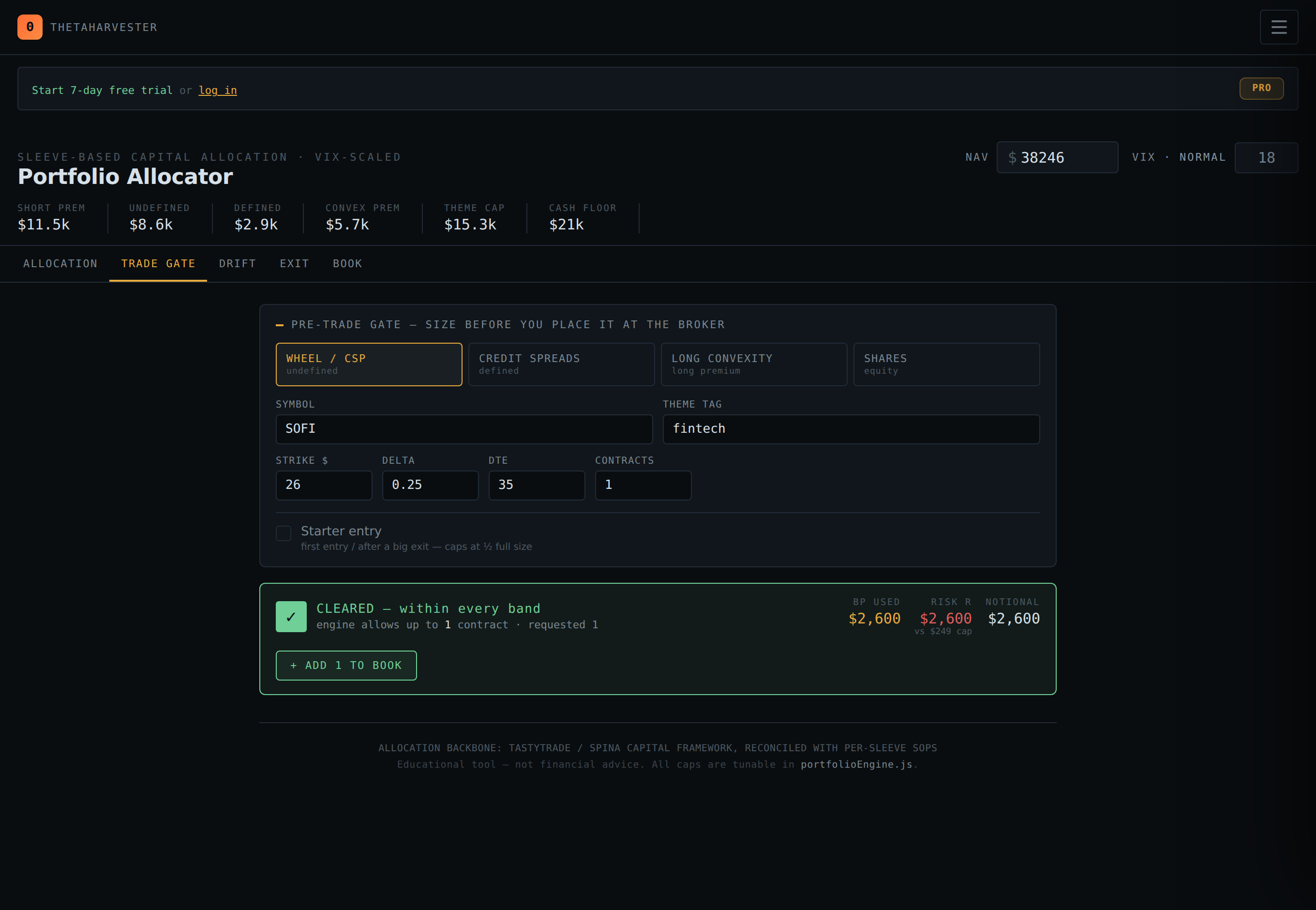

The Trade Gate

The gate tab is where the allocator earns its keep. Describe a proposed trade — sleeve, symbol, theme, strike, delta, DTE, credit — and the engine checks it against the entire book:

- Does it fit the remaining VIX-scaled short-premium budget?

- Does it breach the 40% theme cap — long calls, bull puts, and shares in the same theme all summed together?

- Does full assignment stay under the 15% single-name cap (7.5% for starters)?

- Is the per-position buying power under the 7% (undefined) or 5% (defined) cap?

- For spreads: is the credit at least a third of the width? Is IV rank over 30? Are you already at six concurrent spreads?

- For convexity: is delta at least 0.50 (no OTM lottery tickets), premium within the 2–3.5% of equity band, the underlying liquid and mid-cap or better?

The verdict comes back as hard blocks (the trade violates a binding rule), warnings (outside SOP bands but not fatal), and — most useful — the maximum size that fits. Not "is this trade OK," but "how many contracts does the whole book have room for." Pass the gate and one click adds the position to your book.

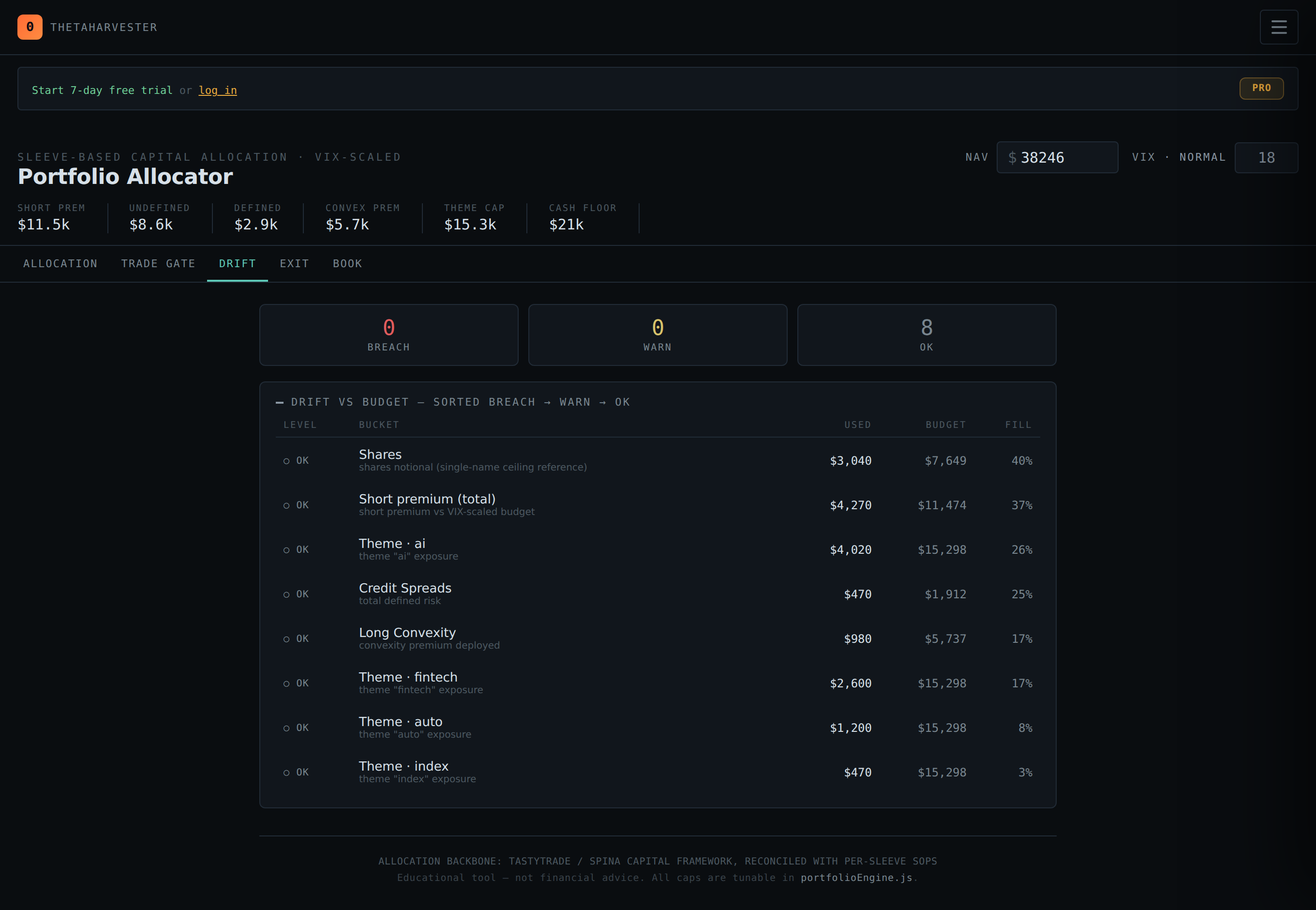

Drift: The Alerts You Actually Need

Budgets are only useful if something tells you when you've drifted past them. The drift panel compares every sleeve's usage against its budget and flags three levels: info (plenty of room), warn (over 90% used), and breach (over budget).

The subtle case is the one the allocator handles best: you didn't trade, but the VIX regime changed. Say the VIX falls from 27 to 14. Your short-premium budget just shrank from 40% of equity to 25% — and a book that was comfortably inside its budget is now over it without a single new position. The engine surfaces exactly how much is over and the trim priority: defined risk first, then undefined, per the tail-risk playbook.

Exit Monitor and Book Editor

Two more tabs round out the engine. The exit monitor tracks every open position against its sleeve's management rules — profit targets hit, time checks due, stops approaching. The book editor is the honest ledger underneath it all: add, edit, and remove positions, or paste in a whole book at once.

Your book lives in your browser and syncs to your account when you're signed in, so the gate and drift checks always run against reality rather than your memory of it.

One NAV, Three Engines

The allocator shares its NAV with Theta Desk — edit it on either page and both re-peg. The desk holds the rules in live dollars; the allocator holds the budgets and checks the book against them; the Wheel Tracker holds the campaign-level cost basis of everything the wheel assigns you.

Same numbers, three angles: rules, budgets, results.

Try It Free

Open the Portfolio Allocator at tharvester.com. Set your NAV and today's VIX, add your open positions to the book, and read the drift panel — most sellers discover their real short-premium allocation is nothing like what they assumed.

Then run your next trade idea through the gate before you place it. The trades the gate blocks are the ones you'll be glad you never made.